Table of Content

This is because the lender will factor in the additional financial responsibility of supporting another person. The more dependants you have, the lower your borrowing power. While having two incomes is advantageous, on a joint application the combined expenses and liabilities the lender considers will be higher, too. Before deciding whether to apply jointly or on your own, be sure to see which method works out the best for your borrowing power. A redraw facility provides a buffer against any future financial hardship by allowing you to access your extra repayments. You can then use these funds for emergencies, such as medical issues or car repairs.

A top up can be used for things like renovations, landscaping, insulation or installing a heating system. Home Loan Experts is a business owned by mortgage broking firm Home Loan Experts Pty Ltd. In order to cool down potentially unsustainable growth in the property market, one of the first levers that the Australian Prudential Regulation Authority pulls is to restrict lending to investors. If you’re unsure of what to enter in the calculator, simply click on the question mark (?) next to the description for further details. Our award-winning mortgage brokers will find you the right home loan for your needs.

How to apply

The calculator will show the maximum amount you can borrow. If you enter your email in the field requested and press ‘SEND’, the calculator will email you a copy of the results. Essential tools and tips on everything from buying to investing in property. Start by figuring out what amount your bank will lend you and, more importantly, what you can afford to borrow. A home loan redraw facility gives homeowners the flexibility to build wealth while reducing debt.

ANZ Home Loans are subject to our lending criteria, terms, conditions and fees. Use this calculator to work out how much you could borrow based on some quick questions about your current financial situation. This is an estimate and is provided for illustrative purposes only. In under 5 minutes, you can get your application started for pre-approvaldisclaimer, a new home loan, refinancing, or topping up your existing home loan. Choosing to repay principal and interest means that, with each repayment, you're paying off interest charges as well as some of the loan principal. Our home loan specialists can help you with pre-approval,disclaimera new home loan, refinancing or topping up your existing home loan.

Living Expenses

We can help you navigate the often complex pre-approval and application process. Our relationships with our panel of lenders allow us to negotiate your interest rate. Of course, you should discuss your situation with your mortgage broker to ensure that you have the right mortgage strategy for your investment plans. Some non-bank lenders aren’t regulated by APRA, which means they don’t need to adhere to serviceability calculation rules.

The first stage of buying a home involves reviewing your finances to understand what you can afford to spend. If you already have a home loan with ANZ you can apply for a top up through the 'Apply and Open' tab in ANZ Internet Banking or goMoney . If you have a home loan with ANZ, you can apply for a home loan top up.

What’s the difference between principal and interest or interest only loans?

The information you submit is subject to our Privacy Policy. Use this tool to calculate the maximum monthly mortgage payment you'd qualify for and how much home you could afford. Gross monthly income is the total amount of money you earn in a month before taxes or deductions. Debt payments are payments you make to pay back the money you borrowed. For a mortgage loan, the borrower often is also referred to as the mortgagor .

The Federal Housing Administration is an agency of the U.S. government. An FHA loan is a mortgage loan that is issued by banks and other commercial lenders but guaranteed by the FHA against a borrower’s default. If you are renting a space, the monthly rent you pay is factored in. The total loan amount, interest, term, and repayment are considered if you have a current mortgage. But if you live with your parents rent-free or are a homeowner, you do not have a repayment or rental expense, which boosts your borrowing power. ' Calculator is only an estimate of how much you may be able to borrow.

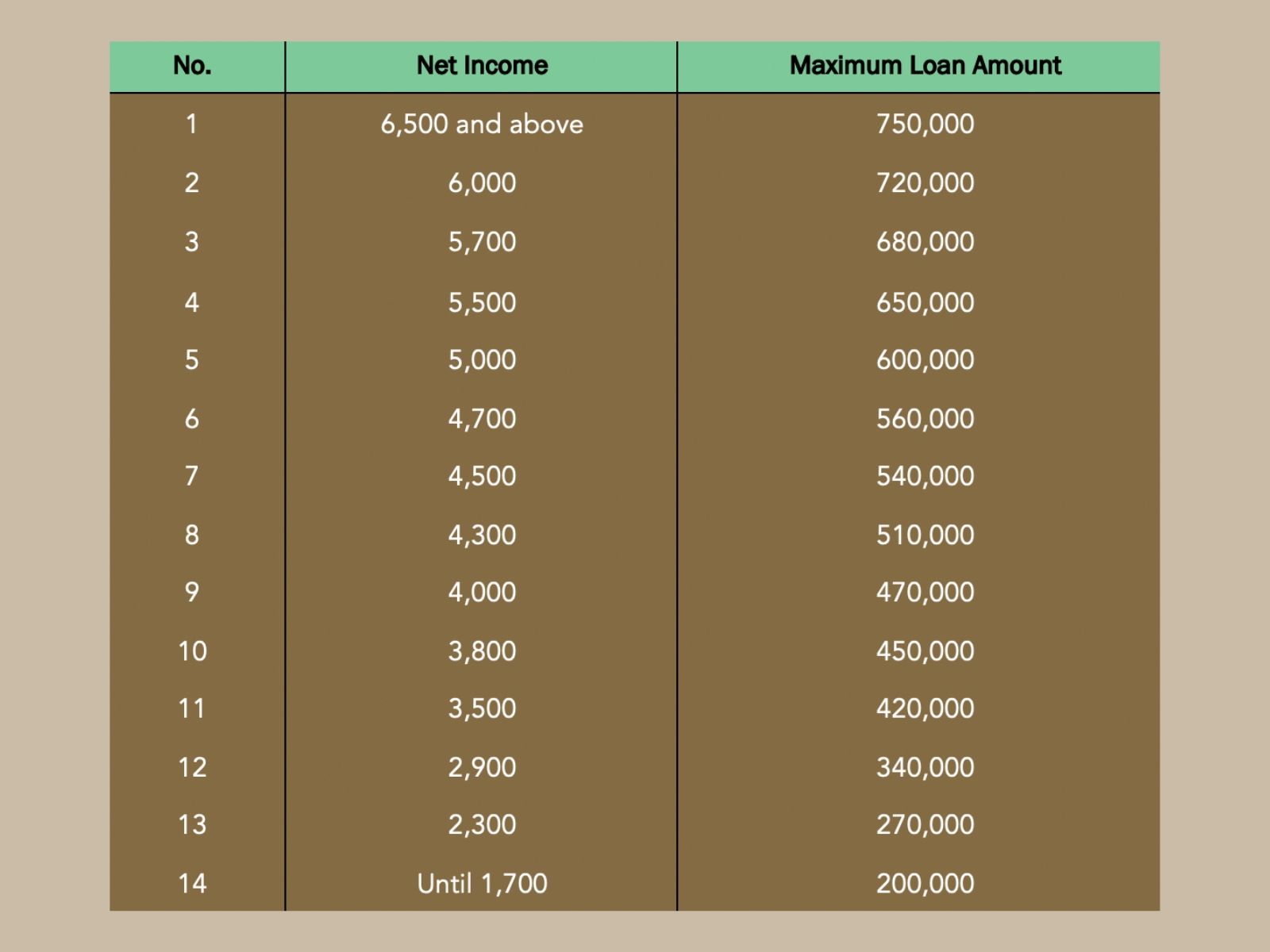

‘How Much Can I Borrow’ Calculator

Get a price range estimatedisclaimerof how much a property could sell for, with options to estimate equitydisclaimerif you already own property. Offer is $4,000 cashback with 80.00% LVR or less, $2,000 cashback for LVR above 80.01%. You must drawdown the Eligible ANZ Home Loan within 120 days from applying. LVR is the amount you're looking to borrow, calculated as a percentage of the value of the property you want to buy. Property value is ANZ's valuation of the security property and may be different to the price you pay for a property. If a Variable Rate Loan is selected, the interest rate will be subject to change throughout the term of the Loan, which can impact on repayment amounts.

In the past, your serviceability was assessed at the actual repayments you would pay every fortnight or month. If you are buying an owner-occupier property, then the lender will not factor in your current rental expense, as this expense won’t exist once you move into the property. The provision of products and services is subject to the laws and regulations of Samoa and ANZ's banking licence in Samoa. Alan Hartstein has worked in publishing for over 25 years as a writer and editor across broadsheets, tabloids, magazines, trade publications and numerous forms of digital content. Alan was initially attracted to journalism through his love of words and their ability to make an impact in the world. Start your home loan pre-approval application in just 5 minutesdisclaimeror find out what a property could sell for,disclaimerso you can buy with more confidence.

Enter the rent that your tenant pays each week, not the rent you receive after agents fees are deducted. If you are are buying an investment property then don\'t forget to add the rental income for the property that you are buying. Fixed-rate home loans lock in a set interest rate, and variable-rate home loans have a rate that moves in line with the standard variable interest rate. Remember also that if you choose to redraw money, the outstanding balance will increase, the amount of interest payable will go up and your minimum repayment amount may also rise. Getting ahead on your mortgage should be the goal of all homeowners as paying it off early means building wealth and reducing debt. At the same time it’s good to know that you can access any funds you’ve accumulated on top of your minimum commitment should you need them, in the form of a redraw facility.

They will check to make sure you can afford your home loan even if you max out your credit cards. But, not every lender assesses your situation in this way and they differ in the repayments they calculate for your credit card debt. Before signing up for a mortgage you should make it clear to your lender that you want a redraw facility and/or an offset account. Just be aware that if you switch from a standard variable rate home loan to a fixed-rate mortgage your redraw options will be limited at best. As their name suggests, fixed rate home loans tend to be quite set in their repayment terms . Fixed rate loans can provide certainty and stability, however you may be charged costs if you want to make additional repayments, pay off your loan early or refinance during the fixed rate period.

No comments:

Post a Comment